Mesothelioma compensation helps patients and families recover costs related to this disease. It covers medical bills, lost wages, and other expenses.

Being diagnosed with mesothelioma is tough. This rare cancer is often linked to asbestos exposure. It can cause high medical costs and financial strain. Seeking compensation can ease this burden. Understanding your options is key. There are several ways to get help, including lawsuits and trust funds.

Each option has its own process and requirements. Knowing where to start can feel overwhelming. But don’t worry, there is help available. This guide will walk you through the steps. It will show you how to pursue the compensation you deserve. Stay informed and take action to protect your future.

Credit: www.asbestos.com

Introduction To Mesothelioma Compensation

Mesothelioma is a rare, aggressive form of cancer. It often develops in the lining of the lungs, abdomen, or heart. It is caused by asbestos exposure. Patients with mesothelioma face many challenges. This includes medical costs, emotional stress, and loss of income. Mesothelioma compensation can help. It provides financial relief and support.

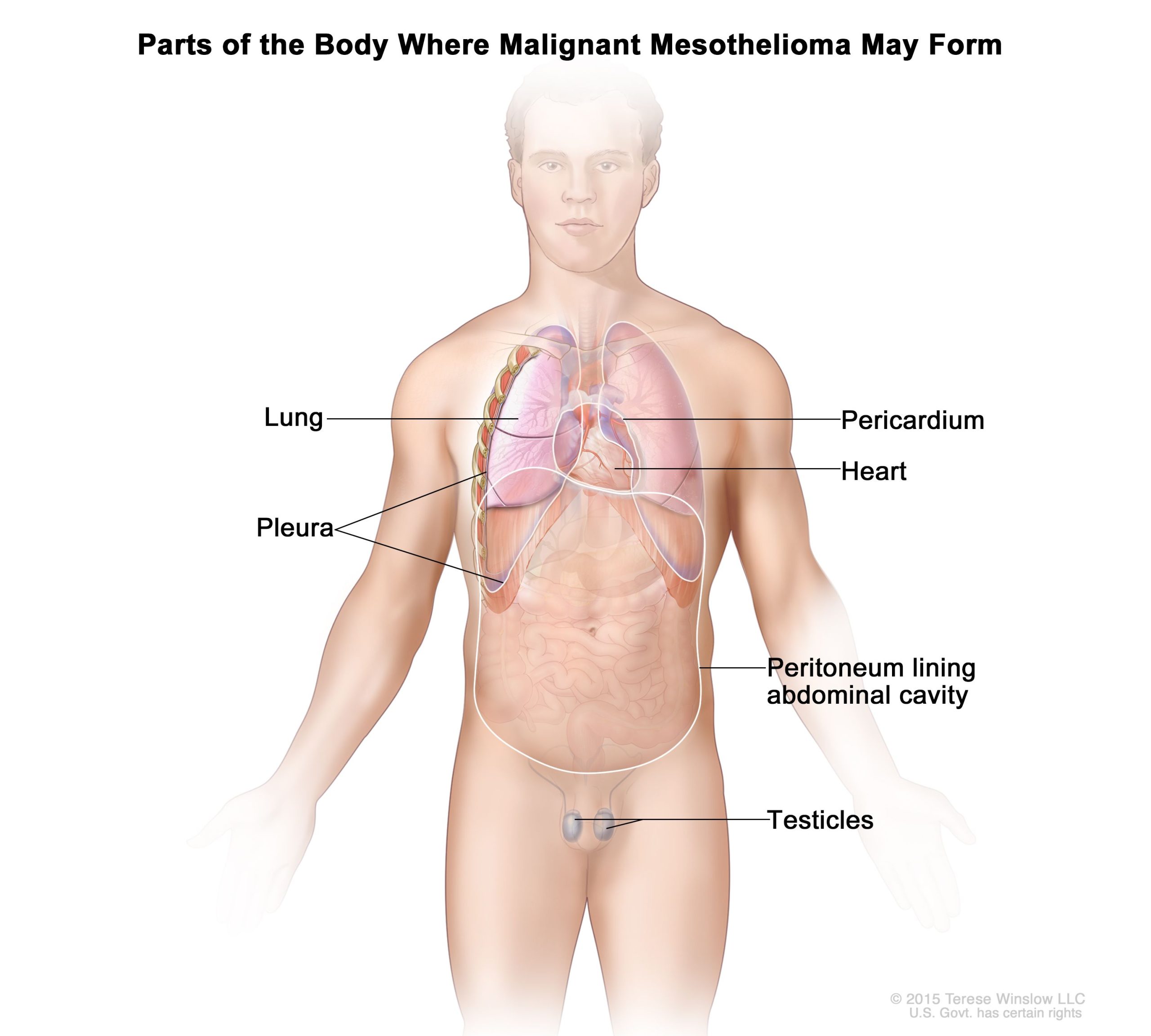

What Is Mesothelioma?

Mesothelioma is a cancer linked to asbestos exposure. Asbestos fibers can be inhaled or swallowed. Once inside the body, they can cause inflammation and scarring. Over time, this can lead to cancer. Mesothelioma primarily affects the lungs. It can also develop in the lining of the abdomen or heart.

There are four main types of mesothelioma:

- Pleural Mesothelioma: Affects the lining of the lungs.

- Peritoneal Mesothelioma: Affects the lining of the abdomen.

- Pericardial Mesothelioma: Affects the lining of the heart.

- Testicular Mesothelioma: Affects the lining of the testicles.

Importance Of Compensation

Mesothelioma compensation is crucial. It helps cover medical expenses. Treatments for mesothelioma are costly. Many patients need surgery, chemotherapy, and radiation. Compensation can ease this financial burden.

Compensation also helps with lost income. Many mesothelioma patients cannot work. They may need to stop working altogether. This loss of income can be devastating. Compensation provides financial support to these families.

Emotional distress is another factor. Mesothelioma affects the whole family. Compensation can help cover therapy and counseling costs. It provides a sense of justice and closure.

Here are some key benefits of mesothelioma compensation:

| Benefit | Description |

|---|---|

| Medical Expenses | Helps cover treatment costs. |

| Lost Income | Provides financial support for families. |

| Emotional Support | Covers therapy and counseling costs. |

Mesothelioma compensation is a vital resource. It supports patients and their families during a difficult time.

Types Of Mesothelioma Compensation

Mesothelioma compensation can be a significant help for victims and their families. Understanding the types of compensation available is essential. Mainly, compensation comes from lawsuits and trust funds. Each type has its own process and benefits.

Lawsuits

Lawsuits can help victims receive compensation for their suffering. There are two main types: personal injury claims and wrongful death claims. Personal injury claims are filed by the patients themselves. These lawsuits seek compensation for medical expenses, lost wages, and pain. Wrongful death claims are filed by the families of deceased victims. These cases seek compensation for the loss of a loved one and related expenses.

Trust Funds

Trust funds are another source of compensation. Many companies set up trust funds to pay asbestos victims. These funds come from companies that went bankrupt due to asbestos-related lawsuits. Victims can apply for compensation from these trust funds. The process is usually quicker and less complicated than lawsuits. Trust funds provide an important financial resource for those affected by mesothelioma.

Eligibility For Compensation

Mesothelioma compensation can provide financial relief for those diagnosed with this serious illness. Compensation helps cover medical bills, lost wages, and pain and suffering. Understanding eligibility for compensation is crucial. This section will guide you through the important criteria and evidence needed to file a claim.

Criteria For Filing

To file for mesothelioma compensation, certain criteria must be met. First, there must be a confirmed diagnosis of mesothelioma. A medical professional must provide this diagnosis. Second, there must be evidence of asbestos exposure. This exposure could have happened at work, home, or other places. Third, the exposure must have occurred in the past.

Time limits apply to filing claims. These limits vary by state. It is important to file within these limits. Seeking legal advice can help understand these time frames. Meeting these criteria is essential for a successful claim.

Evidence Requirements

Providing solid evidence is key to a mesothelioma claim. Medical records confirming the diagnosis are the first piece of evidence. These records should detail the type and stage of mesothelioma. Employment records are also important. They show where and when asbestos exposure happened.

Witness statements can support the claim. Co-workers or others who witnessed the exposure can provide valuable information. Additionally, documenting the impact of the illness on daily life can strengthen the case. This includes medical bills, lost wages, and pain and suffering. Gathering comprehensive evidence increases the chances of receiving compensation.

Legal Process For Filing A Claim

Filing a claim for mesothelioma compensation can be a complex process. It involves several legal steps that require careful attention. Understanding the process helps you prepare and increases your chances of a successful claim.

Finding A Lawyer

The first step in filing a claim is finding a lawyer. A lawyer experienced in mesothelioma cases can guide you through the process. They understand the specifics and have the skills needed to handle your case. Look for a lawyer with a good track record in similar cases. Ask for recommendations and read reviews.

Steps In The Legal Process

Once you have a lawyer, they will start gathering information. This includes your medical history and details of your asbestos exposure. Your lawyer will file the claim on your behalf. They will handle all the paperwork and legal procedures.

Next, the defendant will respond to your claim. They may accept responsibility or deny it. If they deny, your case may go to trial. Your lawyer will represent you in court and present your case.

Sometimes, a settlement is reached before the trial. This means the defendant agrees to pay compensation without admitting fault. Your lawyer will negotiate the best possible settlement for you.

If the case goes to trial, a judge or jury will decide the outcome. If you win, you will receive compensation for your illness. This can help cover medical bills, lost wages, and other expenses.

Compensation Amounts

Mesothelioma compensation amounts can vary greatly. The amount you receive depends on several factors. Understanding these factors can help you know what to expect. This section will discuss the elements that affect compensation amounts and provide average settlement figures.

Factors Affecting Amounts

Several factors influence the compensation amount in mesothelioma cases. These include:

- Severity of illness: More severe cases may result in higher compensation.

- Medical expenses: Costs for treatments and medications impact the amount.

- Lost wages: Compensation considers income lost due to illness.

- Legal fees: Attorney fees are subtracted from the settlement.

- Number of defendants: More defendants can lead to higher settlements.

Each case is unique. Your compensation amount will depend on your specific circumstances.

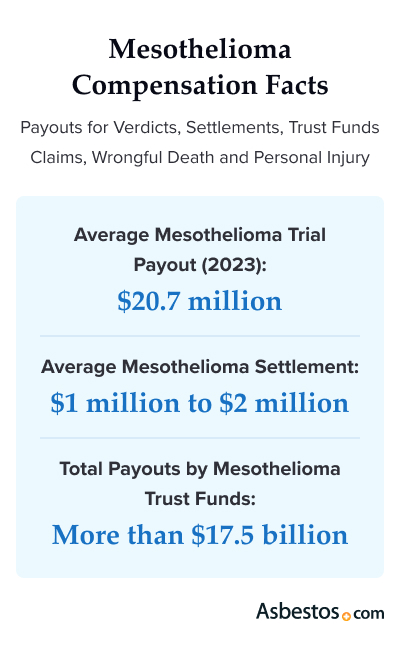

Average Settlements

Average mesothelioma settlements vary. Here are some common figures:

| Type of Compensation | Average Amount |

|---|---|

| Settlement | $1 million to $1.4 million |

| Trial Verdict | $2.4 million |

| Trust Fund Claim | $180,000 |

These figures are averages. Your actual compensation might be higher or lower. Each case is different.

Keep in mind that settlements are generally faster. Trial verdicts may take longer. Trust fund claims can vary based on the fund’s availability.

Expedited Claims

Facing a mesothelioma diagnosis is challenging. Seeking compensation can add stress. Expedited claims can help. These claims speed up the process. They ensure victims get help faster. Read on to learn about fast-track options and requirements.

Fast-track Options

There are several ways to fast-track a mesothelioma claim. Courts understand the urgency. They offer quicker processing methods. Here are some common fast-track options:

- Priority Scheduling: Some courts give priority to severe cases.

- Settlement Negotiations: Many companies prefer to settle quickly.

- Pretrial Conferences: These can streamline the trial process.

- Summary Judgments: Courts may decide cases without a full trial.

Requirements For Expedited Claims

Not all cases qualify for expedited processing. There are specific requirements. Meeting these can help speed up your claim. Key requirements include:

- Medical Documentation: Provide detailed medical records.

- Proof of Exposure: Show evidence of asbestos exposure.

- Financial Hardship: Demonstrate urgent financial need.

- Legal Representation: Hire an experienced attorney.

Meeting these requirements can increase your chances. Ensure all documents are accurate and complete. This minimizes delays and helps the process move faster.

Impact On Financial Future

Mesothelioma can bring significant challenges, not just health-related, but also financial. Compensation claims play a crucial role in securing your financial future. Understanding the impact of compensation can help ease the financial burden and provide peace of mind.

Financial Security

Compensation provides a vital safety net. Medical bills and treatment costs can be overwhelming. Without financial aid, managing these expenses can be challenging. Compensation ensures you can focus on your health without worrying about finances. It covers medical bills, therapies, and other related costs, helping you maintain financial stability.

Long-term Benefits

Receiving compensation offers long-term financial benefits. It supports your family’s future. It can fund ongoing medical care and living expenses. This financial support ensures your loved ones are secure, even in your absence. Compensation can also cover loss of income, ensuring your family can continue to lead a stable life.

Common Challenges And Solutions

Mesothelioma compensation can be a complex process. Patients face several challenges in their pursuit of justice. Understanding these challenges and finding solutions can ease the process. This section highlights common hurdles and ways to overcome them.

Dealing With Denials

Insurance companies often deny mesothelioma claims. They may argue that the disease is not work-related. This can be frustrating for patients and their families. To tackle this, gather all medical records and employment history. Providing detailed documentation can strengthen your case. Consulting with a mesothelioma attorney can also help. They can guide you through the appeal process and ensure your claim is well-supported.

Overcoming Legal Hurdles

Legal processes can be confusing and lengthy. Patients may struggle with understanding legal terms and procedures. It’s crucial to have a knowledgeable attorney on your side. They can explain each step and handle the paperwork. Timing is also important in mesothelioma cases. There are statutes of limitations that vary by state. Filing your claim promptly can prevent delays and ensure your case is heard. Working with a specialized lawyer can make a significant difference in navigating these legal hurdles.

Support Resources

Facing a mesothelioma diagnosis is challenging. Finding the right support resources can ease the burden. This section will guide you through key support resources like legal assistance and financial planning. These resources are vital for mesothelioma patients and their families.

Legal Assistance

Legal assistance is crucial for mesothelioma patients. Experienced lawyers can help you get compensation. They guide you through the legal process. This includes filing claims and lawsuits. They also help gather evidence and represent you in court.

Here’s a brief overview of what legal assistance can offer:

- Case Evaluation: Lawyers assess your case for free.

- Claim Filing: They help file claims with asbestos trust funds.

- Litigation: They represent you in court if needed.

- Settlement Negotiation: They negotiate fair settlements for you.

Financial Planning

Financial planning is another vital support resource. Mesothelioma treatment is expensive. Planning your finances can reduce stress. Financial planners can help you manage your funds. They ensure you have enough for treatment and other needs.

Key services offered by financial planners include:

- Budgeting: Helps you create a budget for medical and living expenses.

- Investment Advice: Guides you on how to grow your savings.

- Insurance Claims: Assists in filing health and life insurance claims.

- Debt Management: Helps you manage and reduce debts.

Utilizing these support resources can make a significant difference. They help you focus on your health and well-being. Don’t hesitate to seek out these valuable services.

Conclusion And Next Steps

Facing a mesothelioma diagnosis is difficult. Seeking compensation can ease financial burdens. This section outlines the conclusion and next steps. It highlights the importance of taking action and securing your future.

Taking Action

Begin by gathering all necessary medical records. Contact a lawyer specializing in mesothelioma cases. They can guide you through the legal process. File your claim as soon as possible. Deadlines for filing vary by state. Quick action ensures better chances of success. Your lawyer will help with paperwork and evidence collection. They will represent you in court if needed.

Securing Your Future

Compensation can cover medical bills, lost wages, and more. A successful claim provides financial security. It helps with ongoing treatment costs. Your family can also benefit from the compensation. It ensures they are taken care of financially. Explore all compensation options available. This includes trust funds and settlements. Discuss these with your lawyer. They will help choose the best path.

Frequently Asked Questions

What Is Mesothelioma Compensation?

Mesothelioma compensation is financial aid for victims of asbestos exposure. It helps cover medical bills, lost wages, and other related expenses. This compensation can be obtained through legal claims or settlements.

Who Can Claim Mesothelioma Compensation?

Individuals diagnosed with mesothelioma due to asbestos exposure can claim compensation. This includes workers, veterans, and family members exposed to asbestos indirectly.

How To File A Mesothelioma Compensation Claim?

To file a claim, consult with an experienced mesothelioma attorney. They will guide you through the legal process, gather necessary evidence, and file the claim on your behalf.

How Long Does Mesothelioma Compensation Take?

Mesothelioma compensation timelines vary. Some claims settle within months, while others may take years. Factors include claim complexity and court schedules.

Conclusion

Securing mesothelioma compensation can provide financial relief and peace of mind. Legal help ensures you receive what you deserve. Remember, time is crucial. Act quickly to protect your rights. Seek advice from experienced lawyers. They can guide you through the process.

Don’t face this journey alone. Support is available. Your well-being matters. Explore your options and take action today.